Introduction

Collective bargaining is a process in which a group of employees negotiate contracts through a union with those who employ them. A union is an organization of workers that collaborate to improve the conditions of their employment. This negotiation between the union and company can cover aspects of employment such as working conditions, pay, and benefits. Collective bargaining agreements (CBAs) are an important aspect of human capital and fall under the “social” aspect of Environmental, Social, and Governance (ESG) reporting.

At the present time there are three sets of proposed standards for reporting collective bargaining agreements. These standards come from the Sustainability Accounting Standards Board (SASB), the Workforce Disclosure Initiative (WDI), and the Global Reporting Initiative (GRI). Each standard concurrently provides overlapping recommendations on disclosures related to collective bargaining agreements, and users can actively apply them together.

Current Proposed Standards for Collective Bargaining Agreements

Sustainability Accounting Standards Board

The Sustainability Accounting Standards Board is a non-profit that works to develop accounting standards for ESG issues. The SASB has issued guidance on the reporting of CBAs. The guidance applies to a variety of industries, such as the food retail and distributor, infrastructure, and transportation industries. The recommended disclosures are the same across industries.

The recommended disclosures are as follows:

- The entity shall disclose the percentage of its employees in the active workforce that were covered under collective bargaining agreements during any part of the reporting period;

- Number and total duration of work stoppages.

Per the SASB standards, companies should disclose the percentage of employees covered by collective bargaining agreements. This percentage should include all employees, whether full-time, part-time, or temporary. Companies should also report the number and length of CBA-caused work stoppages. The SASB recommends disclosing any stoppages that involve more than 1,000 employees or last longer than one full shift. Companies should disclose the length of stoppages in “worker-days idle”, calculated by multiplying the number of employees involved in the stoppage by the hours not worked due to the stoppage.

As an illustration, below are two examples of how companies recently reported this information.

2021 SASB Reports: United Natural Foods Inc. & The Kroger Company

In United Natural Food’s 2021 SASB Report, the company reported the percentage of its active workforce covered by CBAs and the number of work stoppages. The company revealed a 3% decrease in its workforce coverage by CBAs, with 39% of its workforce now covered. There were zero work stoppages during the year, which was a decrease from two stoppages in fiscal year 2020.

Kroger included both recommended SASB disclosures in their 2021 SASB Report. The company reported that CBAs covered 66% of its associates and notes that there were no work stoppages during 2021.

These disclosures present information about workers participating in CBAs and the potential impact of CBAs on a business.

Workforce Disclosure Initiative

The Workforce Disclosure Initiative (WDI) is a platform that aims to enable companies to disclose workforce data involving business operations. Collective bargaining agreements actively govern the relationships between employees and employers, making them an integral part of direct business operations. The WDI provides a survey to help companies show stakeholders more information regarding ESG issues. A section of this survey titled Freedom of Association and Collective Bargaining provides five disclosures related to collective bargaining. These disclosures are the following:

- Describe the company’s process for consulting with workers, their representative bodies and trade unions, as applicable, and other steps to secure workers’ rights to freedom of associate and collective bargaining.

- Provide the percentage (%) of employees covered by collective bargaining agreements for all locations in the company’s direct operations.

- Provide the percentage (%) of employees covered by collective bargaining agreements by each of the company’s significant operating locations.

- How does the company secure the right to collective bargaining of non-employee direct operations workers?

- Has the company identified any risks or restrictions to employees’ right to freedom of association or collective bargaining in any of its direct operations?

The first disclosure is a qualitative explanation of how a company works with workers and unions. Companies should describe “the steps [they take] to gain input from workers, representative bodies and trade unions regarding freedom of association and collective bargaining.” Other important information includes the participants of consultation meetings and how frequently meetings are held.

The second disclosure is a quantitative disclosure of the percentage of a company's direct-business employees in a CBA. A company should disclose this information even if it has no workers that belong to a CBA.

The third disclosure is a broader version of the second, including information for up to 20 significant operating business locations. List each included location and disclose the percentage of employees covered by CBAs at each site.

The fourth disclosure is another qualitative explanation of the steps a business is taking to ensure that non-employee direct operations workers have the right to collective bargaining. Businesses should describe “whether collective bargaining rights are incorporated into [labor] provider contracts… [and] details of any external guidelines or relevant… initiatives which the company supports in line with securing worker rights to collective bargaining.”

The final disclosure is for the company to answer whether they identified risks to their employees’ right to collective bargaining. If the answer is yes, the company should describe “any specific instances where risks or violations have been identified and the process used to identify such risks/violations… [and] actions the company is taking or has taken to address identified risks or violations.”

Centrica is a British energy company. They published a report disclosing the recommended information requested by the WDI in 2021. The section titled Worker Voice and Representation includes the requested information for the five recommended disclosures that relate to CBAs.

Responding to the first disclosure to “describe the company’s process for consulting with workers… to secure workers’ rights to freedom of association,” Centrica disclosed:

We worked with trade unions and supported employed trade union representatives with facilities time and time off, to maintain an open and transparent dialogue. In-person and virtual meetings were held, alongside accessible consultations and negotiations on statutory and voluntary issues at a local and national basis.

In response to the second and third recommended disclosures, “provide the percentage of employees covered by collective bargaining agreements for all locations in the company’s direct operations” and “provide the percentage (%) of employees covered by collective bargaining agreements by each of the company’s significant operating locations,” Centrica disclosed that 71% of its global workforce was unionized. There were two significant operating locations identified, the UK and Europe. The UK had 85% of its workforce covered by CBAs and Europe had 34% of its workforce covered by CBAs.

Responding to the fourth disclosure, “how does the company secure the right to collective bargaining of non-employee direct operations workers,” Centrica disclosed:

We… ensure that third party workers, including those in our supply chain, are enabled to enjoy these same rights through collective rights clauses in supplier contracts as set out in our Responsible Sourcing Policy… Compliance is monitored via our risk processes for supplier onboarding which includes a detailed analysis of labour practice managed by Procurement Managers, and if categorised as higher risk, we undertake further review processes such as undertaking a site inspection or remote worker surveys.

Responding to the fifth disclosure, “has the company identified any risks or restrictions to employees’ right to freedom of association or collective bargaining in any of its direct operations,” Centrica disclosed that there were no risks to its employees right to collective bargaining.

Global Reporting Initiative

The Global Reporting Initiative (GRI) is an independent standards organization that focuses on helping organizations report on ESG related issues. In a document titled GRI 407: Freedom of Association and Collective Bargaining, the GRI outlined its recommended disclosures regarding CBAs. The two recommendations are as follows:

- Management approach disclosures

- Disclosure of operations and suppliers in which the right to freedom of associated and collective bargaining may be at risk.

According to the GRI, management approach disclosures are “a narrative explanation of how an organization manages a material topic, the associated impacts, and stakeholders’ reasonable expectations and interest.”

The purpose of providing management approach disclosures is to give a full disclosure of the organization’s impacts. The particular management approach disclosure for collective bargaining agreements is:

The reporting organization shall report its management approach for freedom of association and collective bargaining. The reporting organization should describe any policy or policies considered likely to affect workers’ decisions to form or join a trade union, to bargain collectively or to engage in trade union activities.

Additionally, disclosures required by the GRI focus on the risk that a company limits its workers ability to collectively bargain:

The reporting organization shall report the following information:

a. Operations and suppliers in which workers’ rights to exercise freedom of association or collective bargaining may be violated or at significant risk either in terms of:

- type of operation (such as manufacturing plant) and supplier;

- countries or geographic areas with operations and suppliers considered at risk.

b. Measures taken by the organization in the reporting period intended to support rights to exercise freedom of association and collective bargaining.

This disclosure helps companies identify areas of weakness in supporting workers' right to associate and collectively bargain. This is especially helpful for multinational corporations that have significant operations in areas with significant restrictions on collective bargaining. The disclosure also allows companies to showcase how they are proactively helping their workers exercise their rights.

The GRI provides guidance on how to identify operations and suppliers that may put workers’ ability to collectively bargain. It also lists several sources that can provide greater insight, including “the various outcomes of the [International Labour Organization] ILO supervisory bodies and the recommendations of the ILO Committee of Freedom of Association.”

American Airlines (Form 10-K, 2021 ESG Report) And Atlas Air (Form 10-K, 2021): Percent of Unionized Workforce

American Airlines (American) is a US-based passenger airline. Atlas Air (Atlas) operates as a major cargo airline and aircraft lessor based in the US. American and Atlas made CBA disclosures in both of their 10-K’s for FY 2021.

At this time, the SEC requires companies to disclose risk factors to their businesses. American and Atlas both disclose their employees’ participation in collective bargaining agreements as risk factors. Disclosures made by both airlines conform to SASB’s standards, particularly the disclosure about the percentage of workers covered by CBAs. At the same time, they do not conform to the GRI or WDI standards.

American

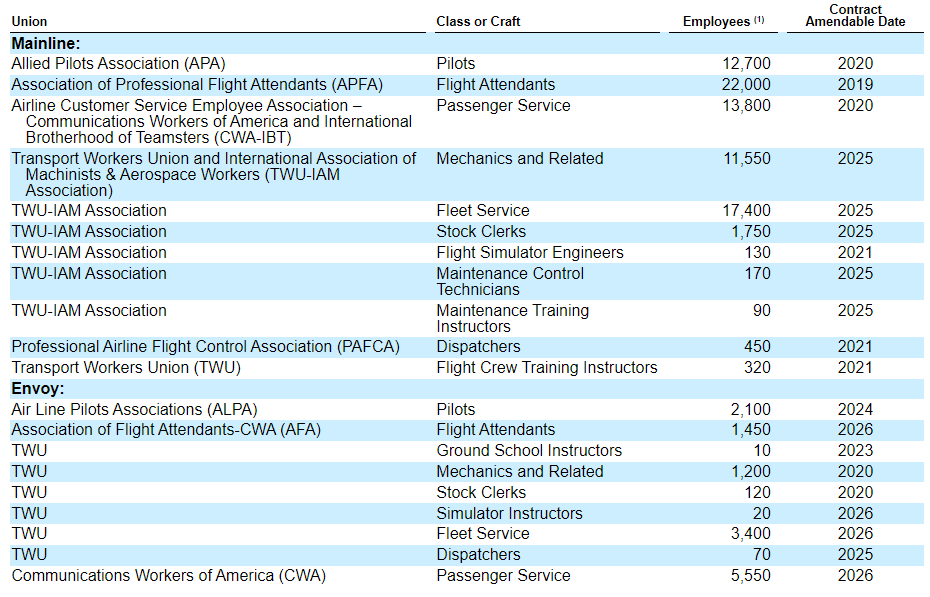

In American’s 10-K, the company disclosed that they had “approximately 123,400 active full-time equivalent employees, approximately 86% of whom were represented by various labor unions responsible for negotiating the collective bargaining agreements (CBAs) governing their compensation and job duties, among other things.”

American disclosed the number of employees associated with each union and the amendable dates for each CBA.

A separate disclosure detailing when major collective bargaining agreements become amendable was also provided:

Joint collective bargaining agreements (JCBAs) covering our mainline pilots, flight attendants, passenger service, flight simulator engineers and dispatchers are now amendable. In January 2022, our mainline flight crew training instructors ratified a three-year agreement which is now amendable in 2025.

In the section of their 10-K titled Risks Related to our Business, American discloses that “Union disputes, employee strikes and other labor-related disruptions, or our inability to otherwise maintain labor costs at competitive levels may adversely affect our operations and financial performance.” The company states that CBAs covering 45% of their employees are amendable or will become amendable within one year. American outlines the process for renegotiating a collective bargaining agreement and discloses current negotiations that could make American’s compensation uncompetitive.

In American’s ESG Report for 2021, the company used the recommended disclosures from SASB to provide information on collective bargaining within the company. American disclosed that CBAs covered 86% of its workforce, and that there were no union work stoppages that year.

Atlas

In Atlas’ 10-K, it discloses important information surrounding collective bargaining agreements. Under the section titled “Human Capital,” Atlas explains that they “have achieved a new five-year collective bargaining agreement (“CBA”) with [their] pilots (“JCBA”).” With this new agreement, Atlas’ pilots would receive higher pay and improved benefits.

In the section of their 10-K titled Risks Related to Our Business, Atlas discloses that “[they] are party to a collective bargaining agreement covering [their] pilots and a collective bargaining agreement covering [their] Atlas and Polar flight dispatchers, which could result in higher labor costs than those face by some of [their] non-unionized competitors.” Atlas explains the details of several of its current collective bargaining agreements in this section, along with the disclosure that they are at greater risk of suffering from increased labor costs and cannot provide any assurance that future labor disputes would result in satisfactory terms for the company.

Under a section titled Labor and Legal Proceedings, Atlas discloses information on three separate collective bargaining agreements, including the terms of the agreements, the date that they become amendable, and a disclosure that Atlas is subject to risks of work stoppage, and could incur extra expenses related to the union representation of their employees.

Dolphin Entertainment Group (SEC Comment Letter Mar. 2015): Disclosing Risks Related To Collective Bargaining

Dolphin Entertainment Group (“Dolphin”) is a public relations company that focuses on the entertainment industry. In a comment letter from the SEC in March 2015, Dolphin was asked to “revise [their] risk factors so that they are narrowly tailored to [their] particular business plan.”

Dolphin acknowledged the SEC’s request and updated their disclosures to include a section titled “Risks Related to the Industry.” The first risk is that union activity has and may continue to adversely affect them in the future.

Dolphin discloses that they “retain the services of actors covered by collective bargaining agreements.” The company explicitly lacks control over the CBA, as it is an industry-wide agreement. Dolphin explains that their ability to retain talent is consequently subject to uncertainties caused by CBAs.

Furthermore, Dolphin discloses that if CBA negotiations fail, the union could engage in strikes, work slowdowns, or work stoppages. These actions could result in delays for Dolphin’s projects. Dolphin is also vulnerable to incurring higher costs from “the renewal of collective bargaining agreements on less favorable terms.” Any changes to collective bargaining agreements could have an adverse effect on Dolphin’s operations.

JetBlue (Q3 10-Q 2019): Increase In Pilots Pay From New Collective Bargaining Agreement

JetBlue is one of the largest airline companies in the United States. During August of 2018, JetBlue entered into a new CBA with the pilot’s union. As a result, wages increased for those pilots. JetBlue explained the wage and salary increase in the following statement in their Q3 10-Q:

Salaries, wages and benefits increased $65 million, or 12.6%, for the three months ended September 30, 2019 compared to 2018. This was primarily driven by the incremental costs of the new pilots’ CBA which became effective on August 1, 2018.

Wages saw an increase of 12.6%, but JetBlue generally attributed this to increased pilot pay from the new CBA.

Hostess Brands (Q2 10-Q 2018): Risks Of Not Renewing Collective Bargaining Agreement

Hostess Brands is a bakery that is famous for snack items, particularly the Twinkie and Hostess Cupcake. Currently, Hostess relies on about 2,000 employees to produce baked goods at a large scale. As a result, the employees formed a union to help represent their interests. However, in 2018 the collective bargaining agreement was ending and Hostess gave the following warning in their Q2 10-Q:

Approximately 46.3% of our employees, as of June 30, 2018, are covered by collective bargaining agreements and other employees may seek to be covered by collective bargaining agreements. Strikes or work stoppages or other business interruptions could occur if we are unable to renew these agreements on satisfactory terms or enter into new agreements on satisfactory terms, which could impair manufacturing and distribution of our products or result in a loss of sales, which could adversely impact our business, financial condition or operating results. The terms and conditions of existing, renegotiated or new collective bargaining agreements could also increase our costs or otherwise affect our ability to fully implement future operational changes to enhance our efficiency or to adapt to changing business needs or strategy.

A CBA covering 14.4% of employees was expiring on December 31, 2018, which was one of Hostess’ main concerns. Hostess wanted to disclose the possible risk of operations slowing down due to strikes because of no new CBA. This disclosure improves shareholders’ comprehension of the potential risks in case of the inability to reach new CBAs with employees.

United Airlines: 2019 Profit Sharing Plan

United Airlines is an international airline based out of the United States and provides services to over 210 destinations. United Airlines’ 2019 Profit Sharing Plan disclosure stated the following regarding employees who fall under the CBA:

Collective Bargaining. As it relates to Qualified Employees who are in the class or craft of employees covered by a collective bargaining agreement with the Employer pursuant to which the Employer has agreed to provide such Qualified Employees with participation in a profit sharing bonus plan, this Plan is maintained pursuant to such agreement.

Employees who fall under the agreement have the option to participate in the profit-sharing bonus plan.

Conclusion

Overall, collective bargaining agreements are an important component of the social pillar of ESG. Companies impacted by collective bargaining agreements should use the recommended disclosures accordingly to inform stakeholders on the potential business effects.

Resources Consulted

SASB - https://s22.q4cdn.com/589001886/files/doc_financials/2021/sr/UNFI_Better_for_All_2021_SASB.pdf

WDI - https://www.centrica.com/media/5325/workforce-disclosure-initiative-response-2021.pdf

https://shareaction.org/investor-initiatives/workforce-disclosure-initiative

GRI - https://www.globalreporting.org/standards/media/1022/gri-407-freedom-of-association-and-collective-bargaining-2016.pdf

https://www.sec.gov/Archives/edgar/data/4515/000000620122000026/aal-20211231.htm

https://www.sec.gov/Archives/edgar/data/1135185/000156459022005515/aaww-10k_20211231.htm