This article discusses proposed disclosures, current guidance, and prevailing regulations that companies must consider as they report their greenhouse gas emissions.

In March 2022, the Securities Exchange Commission released a proposal, The Enhancement and Standardization of Climate-Related Disclosures for Investors, to establish rules that promote clear and consistent climate-related reporting obligations for issuers. The overall proposal discusses potential disclosures related to climate risks in business operations.

This article will discuss the proposed disclosures related to greenhouse gas emission. It will also examine the current guidance and regulations companies follow to report their greenhouse gas emissions.

The major accounting firms have assembled industry task forces to research the implication of this proposal. This article will draw from the guides published as we provide an explanation for companies applying greenhouse gas emissions reporting.

Background Information

Most companies which report their greenhouse gas emissions reference the Greenhouse Gas Protocol (GHG Protocol). This protocol was written by the World Resources Institute and World Business Council for Sustainable Development to measure and manage greenhouse gas emissions from private and public sector operations, value chain, and mitigation actions.

While many consumers are familiar with carbon dioxide emissions (CO2), other GHG emissions are subject to reporting including nitrous oxide (N20), methane (CH4), hydrofluorocarbons (HFCs), and perfluorocarbons (PFCs).

The GHG Protocol defines three different types of GHG emissions:

Scope 1 refers to emissions from operations owned or controlled by a company.

Scope 2 refers to indirect emissions from a company’s purchased or acquired electricity, heating, etc.

Scope 3 refers to emissions from indirect upstream and downstream, also referred to as value chain emissions. This is the most difficult scope to measure due to issues with comparability, double counting, and verifiability. This scope can be broken into fifteen different categories for upstream and downstream activities.

The diagram below illustrates different business activities and designates which scope the respective GHG emissions would fall under. There are different examples of activities for each scope. The categories for Scope 3 are also outlined.

There are different standards and regulations that different companies follow, such as Greenhouse Gas Protocol, Greenhouse Gas Reporting Program, CDP, Environmental Protection Agency, or Intergovernmental Panel on Climate Change.

The EPA has required GHG emission reporting for approximately 41 industries through their Greenhouse Gas Reporting Program (GHGRP). The EPA cites GHGRP’s 40 CFR part 98.2, which requires companies to report their GHG emissions if they are meeting one or more of the following criteria:

A facility that contains any source category such as carbon dioxide, petroleum, ammonia manufacturing, aluminum product, cement production, or other emissions listed in supporting Table A-3 of the regulation.

A facility that emits 25,000 metric tons carbon dioxide equivalent (CO2E) or more per year in combined emissions from applicable source categories.

A supplier listed in supporting Table A-5 of the regulation, such as all producers of coal-to-liquid products, petroleum product suppliers, natural gas and natural gas liquids suppliers, industrial greenhouse gas suppliers, or carbon dioxide suppliers.

Research and development activities are not considered to be part of any source categories.

Low emitters are classified as small businesses, office-based organizations, and public institutions. The majority of their GHG emissions come from purchased electricity and vehicles. The EPA published a specialized Guide to Greenhouse Gas Management for Small Business and Low Emitters.

In addition to required EPA disclosures, companies frequently provide disclosures in sustainability reports and CDP Climate Change Questionnaires. These additional reports may be referenced in their current SEC filings as illustrated by Waste Management's disclosures below.

#1: Waste Management Inc.

remove

add

Waste Management Inc. (WM) is a company that specializes in collection and disposal activities for residential, commercial, industrial, and municipal communities. The following outline demonstrates how WM cites their GHG emissions throughout various annual reports.

10-K

Due to their industry and their high emission levels, WM has reported their GHG emissions to the EPA for years. In their 2021 10-K, they acknowledge their GHG emissions reporting as follows:

We have published our 2021 Sustainability Report, which details the GHG emissions reductions we have facilitated to date and our determination to expand these reductions in the future, as well as our commitment to help make the communities in which we live and work safe, resilient, and sustainable. Our 2021 Sustainability Report can be found at https://sustainability.wm.com, but it does not constitute a part of, and is not incorporated by reference into, this Annual Report on Form 10-K.

This is an example of how a company would report GHG emissions to the public, but not directly to the SEC. All they do is include a comment in their 10-K referring to a different report.

Sustainability Report

The WM’s 2021 Sustainability Report is a public reporting of the company’s data and progress to achieve their sustainability goals. It covers ESG performance aspects, such as climate change, diversity, and retention, for 2020 and early 2021 in accordance with the Global Reporting Initiative. In this report, WM mentions GHG emissions as it pertains to how it avoids emissions to achieve the company’s low carbon goals. The purpose of the data included in this report is stated as:

We report this data to inform our stakeholders of the potential GHG reduction benefits associated with our renewable energy production and the value of the recyclable and compostable materials we collect and process.

The data include communication of efforts WM has implemented to reduce carbon emissions. There are tables illustrating landfill emissions, electricity emissions, and carbon intensity. In addition, this report includes additional comments and explanation on environmental issues WM deems important. One section, discussing landfill emissions states how an acquisition of another company and increase in collection of wastes have contributed to the rise in reported landfill emissions. It continues to discuss what the Company is doing to reduce these emissions:

In 2021, we initiated efforts to design a centralized data management and analytics system that will allow for predictive modeling and targeted investments in operations to drive further emissions reductions.

WM’s sustainability report summarizes and comments on important changes they would like to highlight for investors as it relates to the company’s sustainability. Because WM controls what data they include in this report, it fails to capture all the GHG emissions activity at the company. The sustainability report links to a separate WM website called the data center, which summarized data from CDP Climate Change Questionnaire.

CDP Climate Change Questionnaire

The CDP Climate Change Questionnaire, as mentioned above, is a disclosure system for entities to manage their environmental impacts. This expands on emissions data in a format that goes more in depth with each scope’s emission level, different gases used, and different regions and countries. WM cites the following as methodologies it uses in collecting activity data and calculating emissions:

IPCC Guidelines for National Greenhouse Gas Inventories

2006 The Climate Registry: General Reporting Protocol

The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (Revised Edition)

The Greenhouse Gas Protocol: Scope 2 Guidance

US EPA Mandatory Greenhouse Gas Reporting Rule

Companies have various direct operations that result in Scope 1 emissions. WM’s scope 1 emissions come from direct operations like landfill, collection fleet, etc. Categories of scope 2 and scope 3 emissions are standardized across all companies. This report includes an outline of information for each scope. This outline can be seen below:

In addition, another section further analyzes the scope 1 emission data by breaking down by greenhouse gas types, by country/region, and by business division. The same data can be seen for Scope 2 and 3. The data is outlined as seen below:

WM is an example of a company’s thorough compilation and reporting of GHG emission data. The company disclosures in SEC filings, in the Sustainability Report, and in the CDP Climate Change Questionnaire are all important for different audiences but rely on and report similar information about WM’s GHG emissions.

SEC Proposal

The SEC proposed that US 10-K filers and foreign private issuers who file 20-F forms will need to disclose their GHG emissions. This information would be included in audited financial statements, such as financial impact metrics, expenditure metrics and financial estimates and assumptions, etc., and a newly created section of each respective form immediately before the management’s discussion and analysis section. Larger companies would have to disclose most of this information as of fiscal year 2023, while smaller companies could wait until fiscal year 2024.

Among other climate related disclosures, the new SEC rule includes requirements to report GHG emissions. Registrants would disclose information for their emissions under scope 1 and 2. Scope 3 would only need to be disclosed if material or if the filer has a target goal to reduce emissions.

Registrants would need to disclose emissions disaggregated by each scope and constituent greenhouse gas (e.g. carbon dioxide, methane, nitrous oxide, nitrogen trifluoride, hydrofluorocarbons, perfluorocarbons, and sulfur hexafluoride) and in the aggregate. Additional information would need be disclosed regarding the intensity per unit of production terms, methodology, significant inputs, and significant assumptions used in calculations.

Registrants would also need to provide a statement by an independent attestation service provider to verify the accuracy and completeness of the emission reporting.

The following image from KPMG’s guidance on the SEC proposal illustrates the before the management discussion and analysis section:

The following image from KPMG shows a timeline of proposed disclosure and assurance requirements for each scope according to different filer statuses.

This proposal would also impact initial public offerings. The same disclosures would not have a scope exception for companies filing registration statements in connection with the registration of a security, a security offering, or an investment company. However, a new registrant would not be required to obtain assurance over its GHG emissions during an IPO.

There are many similarities between this new SEC proposal and the GHG Protocol and GHGRP. The SEC cites the same definitions for the emission scopes and greenhouse gases. The SEC also requires the metric carbon dioxide equivalent to ensure comparability across registrants and achieve the overall SEC goal of promoting clear and consistent reporting. With the similarities between what the SEC is anticipating and existing guidance, many companies will be able to easily transfer their reporting.

#2: Microsoft Inc.

remove

add

Microsoft Inc is a software company that specializes in production of computer software and consumer electronics. Microsoft’s GHG emissions reporting is similar to the guidelines in the SEC’s proposal.

10-K

In their 2022 10-K, Item 1 includes a section Corporate Social Responsibility with subsection Commitment to Sustainability. In their filing, Microsoft references GHG emissions as follow:

With an overall reduction in our combined Scope 1 and Scope 2 emissions, our Scope 3 emissions increased, due in substantial part to significant global datacenter expansions and growth in Xbox sales and usage as a result of the COVID-19 pandemic. Despite these Scope 3 increases, we will continue to build the foundations and do the work to deliver on our commitments, and help our customers and partners achieve theirs. We have learned the impact of our work will not all be felt immediately, and our experience highlights how progress won’t always be linear.

In addition, Microsoft cited disclosures about carbon removal emissions, new zero waste certifications, and purchases of removal carbon. This is a summary of the data, which can be found in Microsoft’s Sustainability Report.

Sustainability Report

Microsoft’s 2021 Environmental Sustainability Report gives a thorough review of the GHG emissions in their Appendix D Section 1.1. This includes majority of the information that would be required according to the SEC’s proposal. First, Deloitte & Touche LLP completed an independent accountant’s review report that verifies the GHG emission data as follows:

We have reviewed management of Microsoft Corporation’s (the “Company”) assertion that the specified information included in Section 1 of Appendix D of the accompanying 2021 Environment Sustainability Report (Appendix D) as of and for the fiscal year ended June 20, 2021 is presented in accordance with the criteria set forth in Section 1.10, Reporting criteria in Appendix D. The Company’s management is responsible for its assertion.

Section 1.9 of Appendix D discusses the methodology for each scope. Scope 1 and 2 involved looking at primary data, while Microsoft’s calculations for scope 3 were more extensive and dealt with supplier data percentage. Each scope 3 category has its own emissions calculation methodology and emission factors used.

The report outlines the following activities under each scope:

Scope 1 – fossil fuel combustions, executive air travel, ground transportation (Microsoft owned and directly leased)

Scope 2 – purchased electricity, chilled water, and steam

Scope 3 – purchased goods and services, capital goods, fuel and energy related activities (location based and market based), upstream transportation, waste, business travel, employee commuting, downstream transportation, use of sold products, end of life of sold products, and downstream leased assets.

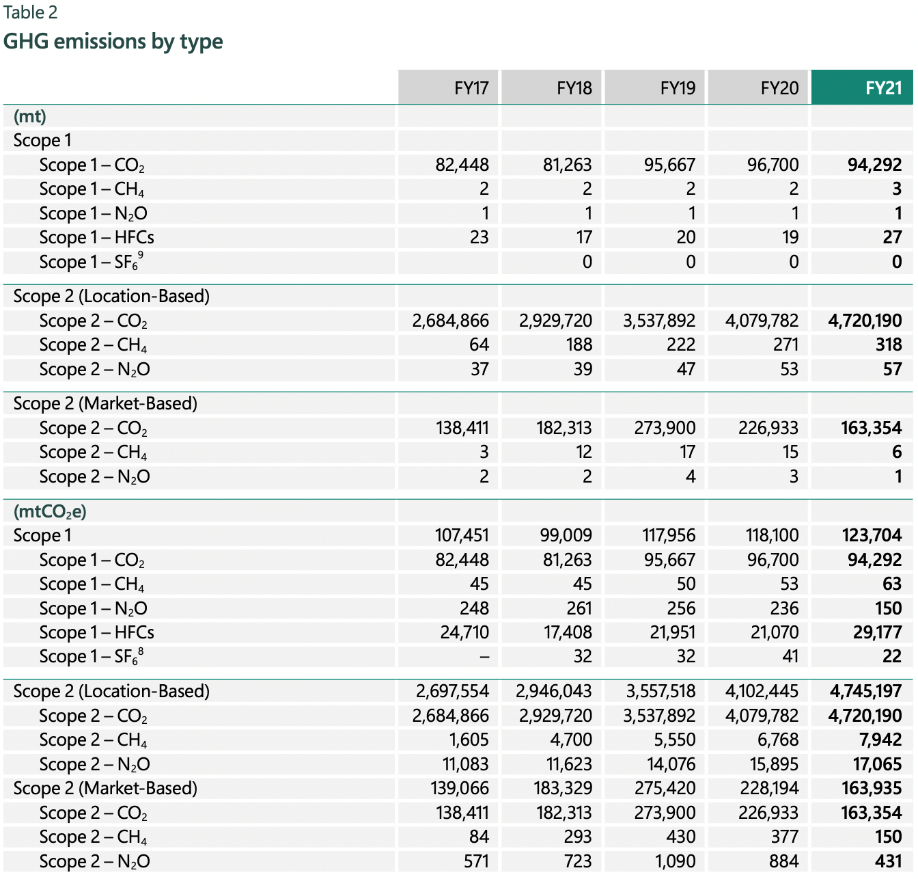

As for the data, Microsoft states that GHG emissions are presented in accordance with the GHG Protocol and GRI Standards. They present their data in tables, and it relates the SEC’s required GHG emission data. These tables also extend to previous years where Microsoft also calculated their GHG emissions:

The tables provide clear communication and outline the important information for gas emissions in each scope and gas. The carbon intensity is used as a measurement for a company to calculate the emission rate for a specific activity. In this example, the GHG emissions intensity is calculated as metric tons of carbon dioxide equivalents emitted per million dollars of revenue.

Conclusion

GHG emissions are one of the main aspects of ESG reporting for which the SEC has proposed clear and consistent reporting requirements. While the proposal has not been officially passed, these are the general aspects that may be adopted in the future. Companies should begin to anticipate and implement necessary processes to how they should gather, record, and report their GHG emissions.

.png)